Are you feeling overwhelmed by mounting debts and considering bankruptcy as your only way out? Before taking this drastic step, it’s crucial to explore the various solvency assistance programs available.

These programs provide hope and practical solutions for individuals and businesses in financial distress, offering a recovery path without the long-lasting consequences of bankruptcy.

In this article, we’ll dive into the world of solvency assistance. It can help you regain financial stability. It also offers alternatives that could transform your future and bring back peace of mind.

Contents

- 1 Financial Stability and Bankruptcy

- 2 Government Assistance Programs

- 3 Non-Profit Organizations and Charities

- 4 Negotiating with Creditors

- 5 Developing a Personal Financial Recovery Plan

- 6 Building Financial Resilience for the Future

- 7 The Role of Professional Financial Advice

- 8 Monitoring Progress and Adjusting Strategies

- 9 Conclusion

- 10 Frequently Asked Questions

Financial Stability and Bankruptcy

Solvency and insolvency represent opposite ends of the financial stability spectrum. Solvency indicates that an entity can meet long-term financial obligations, maintaining a healthy balance between assets and liabilities. Insolvency occurs when financial obligations can’t be met, often leading to bankruptcy if left unaddressed.

Recognizing signs of approaching insolvency, such as consistently late payments or maxed-out credit lines, allows for early intervention. However, if bankruptcy becomes necessary, it carries significant consequences. The most immediate is severe damage to credit scores, with bankruptcy remaining on credit reports for up to 10 years. This makes securing loans, credit cards, or favorable interest rates challenging.

Bankruptcy may require liquidating assets to repay creditors, potentially resulting in the loss of valuable possessions. Post-bankruptcy, financial options become limited, hindering personal and professional growth. The process can also be emotionally draining, leading to anxiety, depression, and strained relationships due to the associated stigma and stress.

Exploring Solvency Assistance Programs

Given the severe consequences of bankruptcy, it’s crucial to explore alternatives. Solvency assistance programs offer structured support, guidance, and education to help individuals and businesses manage debt and improve their financial situation. Key components include credit counseling, debt management plans, and financial education workshops.

Debt consolidation, another approach within solvency assistance, involves combining multiple debts into a single loan with a lower interest rate, simplifying financial obligations, reducing overall interest rates, and aiding faster debt repayment and financial stability.

Debt is a significant issue in many American states, with individuals and families often struggling to manage credit card balances, student loans, mortgages, and other financial obligations. Michigan, in particular, has seen its residents grappling with financial difficulties due to various economic challenges. The state’s industrial background and recent economic shifts have contributed to a complex financial landscape for many of its residents.

Understanding the specific needs and circumstances of Michigan residents is essential when seeking effective debt relief solutions. Numerous programs are available, with affordable Michigan debt relief options tailored to the specific needs of its residents. These debt relief programs Michigan are designed to provide practical solutions that address the unique economic conditions of the state, offering hope and a path toward financial stability for those in need.

Solvency assistance programs are essential tools for those facing financial distress, offering a range of services from credit counseling to debt consolidation. By taking advantage of these programs, individuals can gain a clearer understanding of their financial situation and develop personalized plans to address their debt. These programs play a critical role in helping individuals regain control of their finances and avoid the severe consequences of bankruptcy.

| Feature | Bankruptcy | Solvency Assistance Programs |

| Credit Score Impact | Severe, long-lasting | Moderate, shorter-term |

| Asset Protection | Limited, may require liquidation | Generally protected |

| Debt Forgiveness | Possible, depends on the type | Varies by program |

| Duration | 7-10 years on credit report | Typically 3-5 years to complete |

| Future Credit Access | Severely limited | Gradual improvement |

| Cost | High legal and filing fees | Lower fees, some programs free |

| Flexibility | Limited options | Various programs available |

Government Assistance Programs

Government agencies at federal, state, and local levels offer a variety of assistance programs designed to help individuals and businesses avoid bankruptcy and regain financial stability.

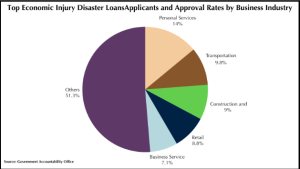

The Small Business Administration (SBA) plays a crucial role in supporting small businesses facing financial difficulties. Their Economic Injury Disaster Loans (EIDL) provide low-interest funds to small businesses experiencing substantial economic injury due to declared disasters.

The SBA Debt Relief Program offers immediate assistance by covering principal, interest, and fees for existing SBA loans for a specified period. For homeowners struggling with mortgage payments, government-backed programs provide relief and help prevent foreclosure.

The Home Affordable Modification Program (HAMP) assists in modifying mortgages to make monthly payments more affordable, potentially reducing interest rates, extending loan terms, or even forgiving a portion of the principal balance.

The Home Affordable Refinance Program (HARP) allows homeowners with little or no equity to refinance their mortgages at lower interest rates, potentially reducing monthly payments and improving overall financial stability.

The Department of Housing and Urban Development (HUD) offers housing counseling services to help individuals and families facing housing-related financial challenges. These services include advice on preventing foreclosure, renting, and managing credit issues.

Additionally, many states and local governments have their own assistance programs, offering grants, low-interest loans, or financial counseling services to residents facing financial hardship. These programs often target specific needs such as utility bill assistance, job training, or emergency financial aid.

Non-Profit Organizations and Charities

Non-profit organizations and charities play a vital role in providing financial assistance and support to individuals and families facing economic hardship. These organizations offer a wide range of services designed to address both immediate financial needs and long-term stability.

Many organizations provide emergency financial assistance for essential expenses such as rent, utilities, or medical bills, helping prevent evictions or utility shutoffs that could exacerbate financial struggles. Food banks and housing support programs operated by non-profits help ensure that basic needs are met, allowing individuals to focus on addressing their broader financial challenges.

Job training and employment services offered by these organizations can be crucial in helping people increase their income and improve their long-term financial outlook. Many non-profits also provide financial literacy education, teaching essential skills like budgeting, saving, and understanding credit.

Some charities specialize in providing specific types of assistance, such as helping with medical debt or offering micro-loans to help individuals start small businesses. Others focus on particular demographics, such as veterans, single parents, or the elderly, tailoring their services to meet the unique needs of these groups.

Many non-profits also act as advocates, helping individuals navigate complex government assistance programs or negotiate with creditors. By leveraging the resources provided by these organizations, individuals can address immediate financial needs while working towards long-term stability.

The holistic approach taken by many non-profits, addressing not just financial issues but also related challenges like healthcare, education, and employment, can be instrumental in helping people break the cycle of financial instability and build a more secure future.

Negotiating with Creditors

One often overlooked strategy for avoiding bankruptcy is direct negotiation with creditors. Many creditors are willing to work with individuals facing financial difficulties, as they prefer to receive partial payment rather than risk receiving nothing through bankruptcy proceedings.

Debt settlement involves negotiating with creditors to accept a lump sum payment that is less than the full amount owed. While this approach can significantly reduce your overall debt burden, it’s important to consider the potential impact on your credit score and tax implications.

Some creditors may be willing to lower your interest rate temporarily or permanently, making it easier to manage your monthly payments and pay down your debt more quickly. Additionally, creditors may agree to revised payment plans that better align with your current financial situation, including lower monthly payments, extended repayment terms, or even temporary payment deferrals.

Developing a Personal Financial Recovery Plan

While solvency assistance programs can provide valuable support, long-term financial stability requires a comprehensive personal recovery plan. The foundation of any financial recovery plan is a realistic and sustainable budget. This involves tracking all income and expenses, identifying areas for potential cost-cutting, prioritizing essential expenses and debt repayment, and allocating funds for savings and emergency reserves.

Exploring opportunities to increase your income can accelerate your path to financial stability. Consider seeking a higher-paying job or negotiating a raise, taking on part-time or freelance work, monetizing skills or hobbies through side businesses, or selling unused items or assets.

Establishing an emergency fund is crucial for long-term financial stability. Aim to save 3-6 months of living expenses to provide a buffer against unexpected financial setbacks. Additionally, investing time in improving your financial knowledge can help you make better decisions and avoid future financial pitfalls.

Take advantage of free resources such as online financial education courses, personal finance books and podcasts, and workshops offered by local financial institutions or community organizations.

Building Financial Resilience for the Future

While addressing immediate financial challenges is crucial, building long-term financial resilience is equally important. This involves developing habits and strategies that protect you from future financial crises. Start by diversifying your income streams to reduce reliance on a single source of income. This could include developing multiple skills, investing in passive income opportunities, or starting a side business.

Create a robust savings plan that goes beyond emergency funds, including long-term goals like retirement. Educate yourself about various investment options and consider working with a financial advisor to develop a diversified investment portfolio aligned with your risk tolerance and financial goals.

Regularly review and update your insurance coverage to ensure you’re protected against potential financial setbacks. This includes health, life, disability, and property insurance. Finally, make financial education a lifelong pursuit. Stay informed about economic trends, tax laws, and personal finance strategies to make informed decisions and adapt to changing financial landscapes.

The Role of Professional Financial Advice

Professional financial advice is crucial in navigating complex financial situations and avoiding bankruptcy. While solvency assistance programs offer valuable support, personalized guidance from financial professionals can provide tailored solutions to your specific circumstances. Certified financial advisors bring expertise in debt management, investment planning, retirement savings, and tax optimization.

A financial advisor can help develop a comprehensive plan to address current challenges while working toward long-term stability. They can objectively assess your situation, identify pitfalls, and suggest strategies you might not have considered.

Consulting with a bankruptcy attorney can provide insights into your options and the consequences of different financial decisions. They can help you understand the pros and cons of bankruptcy versus alternatives, your rights and obligations, and potential impacts on your assets and future opportunities.

Tax professionals can play a vital role, especially when dealing with tax debt or debt settlement options. While professional advice comes at a cost, the long-term benefits often outweigh the initial expense. Many professionals offer initial consultations at reduced rates or for free, allowing you to assess their value before committing.

Monitoring Progress and Adjusting Strategies

Continuous monitoring and adjustment of financial strategies are crucial for successful recovery and avoiding bankruptcy. Regularly assess your progress by setting clear, measurable milestones such as paying off specific debts or improving your credit score.

Review your budget and spending habits frequently, as financial circumstances can change rapidly. Be prepared to reassess expenses, identify new savings opportunities, and adjust allocations based on changing priorities.

Evaluate the effectiveness of your debt repayment strategies, considering alternatives if current methods aren’t yielding the expected results. Regularly track your credit score and review your credit report for insights into your financial health.

Celebrate small achievements to maintain motivation, but be ready to adjust goals and strategies when faced with unexpected setbacks. Stay committed to long-term financial health through ongoing education about new financial products, tax law changes, and economic trends.

By consistently monitoring progress, remaining flexible, and staying informed, you can navigate financial recovery more effectively and build lasting financial stability.

Conclusion

Avoiding bankruptcy and achieving solvency is not just about addressing immediate financial challenges. It requires a long-term commitment to financial responsibility and continuous learning. You can deal with financial distress by using solvency programs.

You can also recover by making a financial plan. And by sticking to long-term financial health. Remember that seeking help early and being proactive can prevent financial challenges. They are key to avoiding bankruptcy and building a secure future.

Frequently Asked Questions

How long does it typically take to complete a Michigan debt relief program?

Most Michigan debt relief programs last 3-5 years, depending on your debt amount and financial situation. However, some may be shorter or longer. The goal is to pay off debts while learning better financial habits.

Are solvency assistance programs, such as MI debt relief, available for small businesses in Michigan?

Yes, there are programs specifically designed to help small businesses in Michigan avoid bankruptcy and regain financial stability, including MI debt relief. These include SBA loans, debt restructuring services, and financial counseling tailored to business needs. Local economic development agencies may offer additional resources.

Can I still use credit cards while enrolled in a debt management program?

Most programs require you to close credit card accounts, but some may allow you to keep one for emergencies. The focus is on breaking the cycle of credit card debt and learning to live within your means.